Options Trade #20 - SPY Long Straddle

Sep 19, 2018VTS Community,

* There's a new trade in VTS Discretionary today, details below. But I want to follow up a bit on yesterday's blog. Sorry for the long email today :)

Yesterday's blog about factoring in days to expiration in our VIX futures term structure levels was popular. For those that missed it, the video is here, and I had a bunch of "oh I didn't know that" type of follow-ups. Thanks for all the kind words about how much I share.

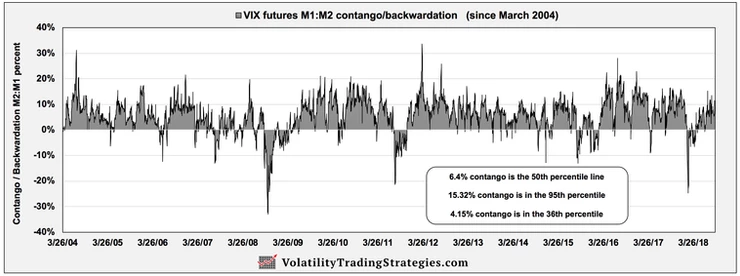

To follow up, the M2:M1 contango level was 4.15% at the open today. Now it's important to note, the VIX itself was down 6% at the open as well so volatility has dropped quite a bit today. Contango was only 3% in early trading when the S&P futures were flat, and could easily have been well below that if markets were down.

VIX futures closed yesterday 15.32% in contango - This value is in the 95th percentile of all past values

VIX futures opened today 4.15% in contango - This value is in the 36th percentile of all past values

So volatility dropped substantially, yet contango levels went from their 95th percentile to only the 36th percentile? From 15 to 4?

Clearly, if the VIX futures are to be useful as indicators, we need to normalize these data points to avoid dramatically different trade signals based on nothing but a technicality. And this is true of all the other volatility indicators as well. Looking at static values can give a very inadequate picture of the overall situation. It would be like measuring economic data without adjusting for inflation. That can lead to some very big oops moments, but with volatility, as we've seen in the past oops moments and data mistakes can be very costly indeed.

* New VTS Discretionary Strategy trade #20 today

With the S&P 500 right at all-time highs, these are the times that I like to take a shot at trades that benefit from larger moves in either direction. I can imagine stocks continuing to climb here, or due to some upcoming headwinds (Fed meeting, Midterm elections), I can see stocks pulling back as well. And since volatility has declined today, it's a good entry point for a long Straddle.

The Trade:Long Straddle on S&P 500 (SPY)

- BUY to OPEN 2 x 16 Nov 18' 291 Put

- BUY to OPEN 2 x 16 Nov 18' 291 Call

- Debit: ~ 9.24

* prices move around so do the best you can, the lower the better

Margin Requirement: - 1 option contract = 100 shares if assigned - We're paying a debit of 9.24 - This trade requires 924 in margin per contract - The model portfolio is opening 2 contracts, so 1848 margin

- The VTS Discretionary model portfolio is at 26,035.35 - 1,848 is 7.1% of the portfolio capital

* You can scale your trade to roughly 5-10% of your VTS Discretionary funds. We keep long straddles quite small.

Stop-loss: - We always use a 10% stop-loss on this type of trade - 924 per contract is what the trade is valued at - 924 * 10% = 92.4

* If we are down more than 92$ per contract we will close it

Take Control of your Financial Future!

Profitable strategies, professional risk management, and a fantastic community atmosphere of traders from around the world.