VXZ vs 1/2 VXX to Profit from a Market Crash

Mar 12, 2026VTS Community,

This Iran War is quite a serious event that will likely change the course of history, at least in the short to medium term. Having said that, it hasn't yet materialized into the most extreme Volatility readings to a level that would push us into a Long Volatility position in the Tactical Rotation Strategy. There's still some risk of that if things take a turn for the worse, but so far we have just maintained our safety Gold position.

If and when we do move into Long Volatility it will be with the Volatility ETP VXZ, or the materially identical VIXM. Price wise they track the exact same VIX futures, it's just one of them is an ETN and one is an ETF. Both totally safe, no issue to use either.

A VTS member with a very large trading account is concerned about potential liquidity, so the question is:

Are there any replacements for VXZ / VIXM?

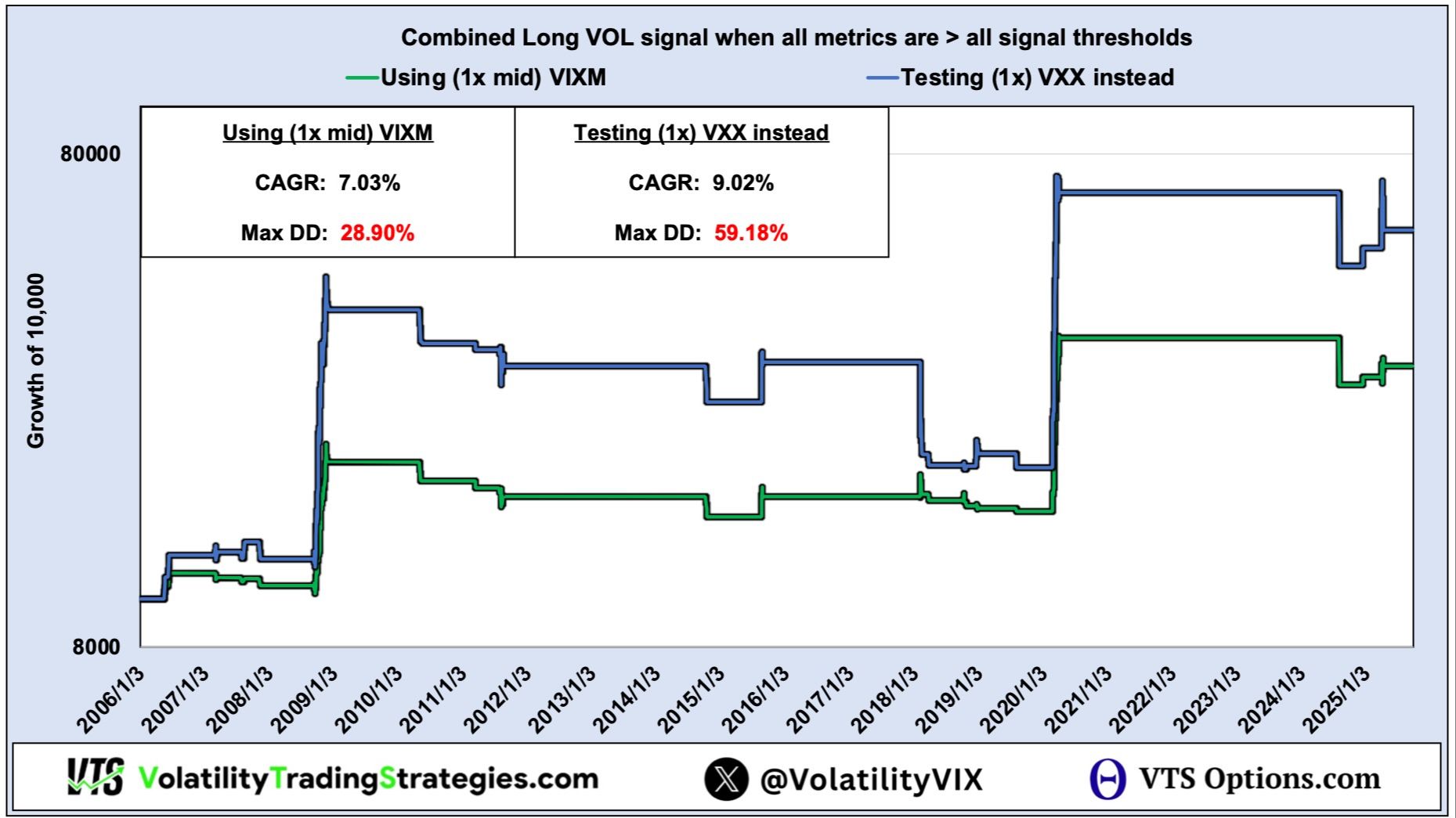

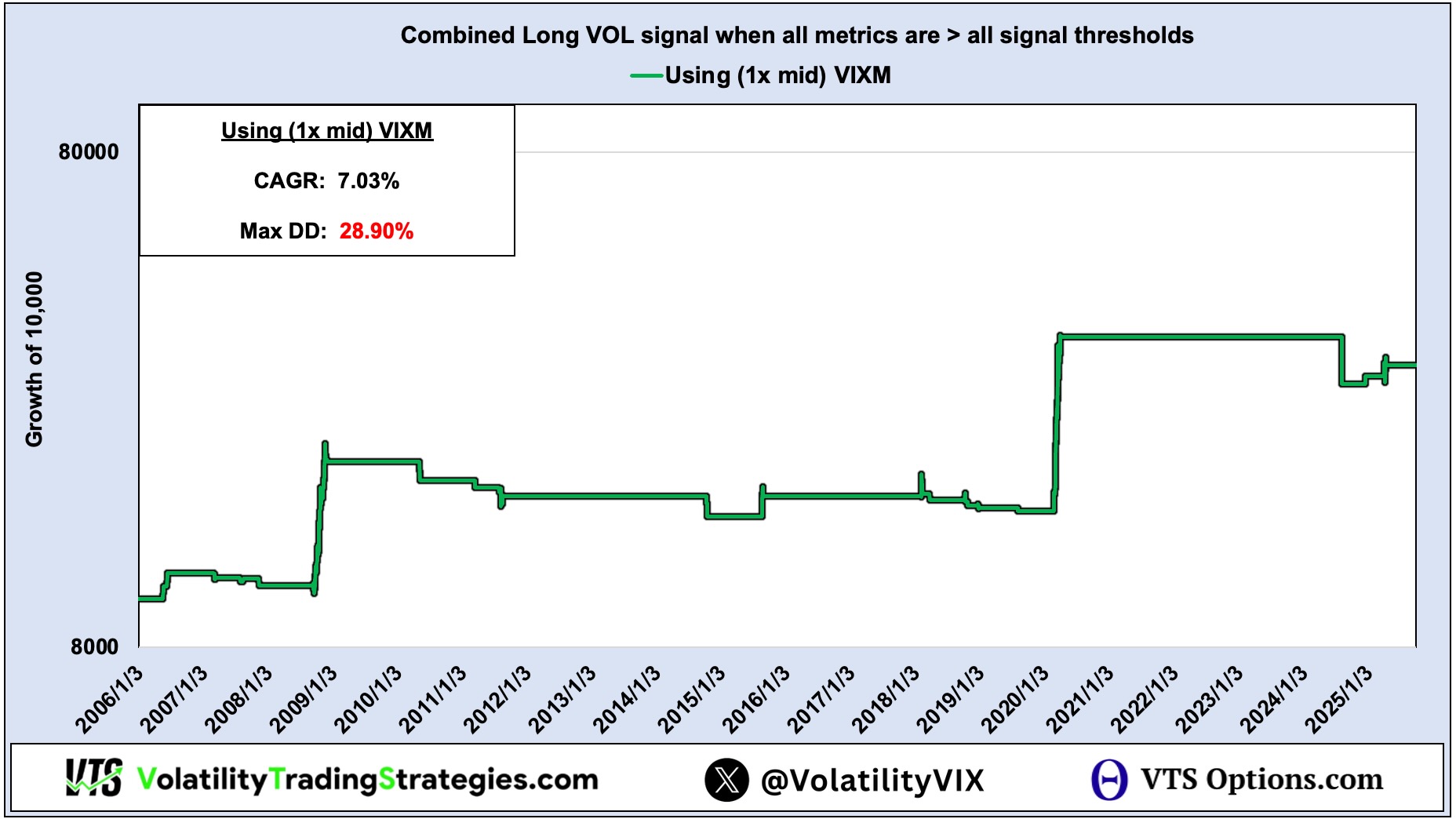

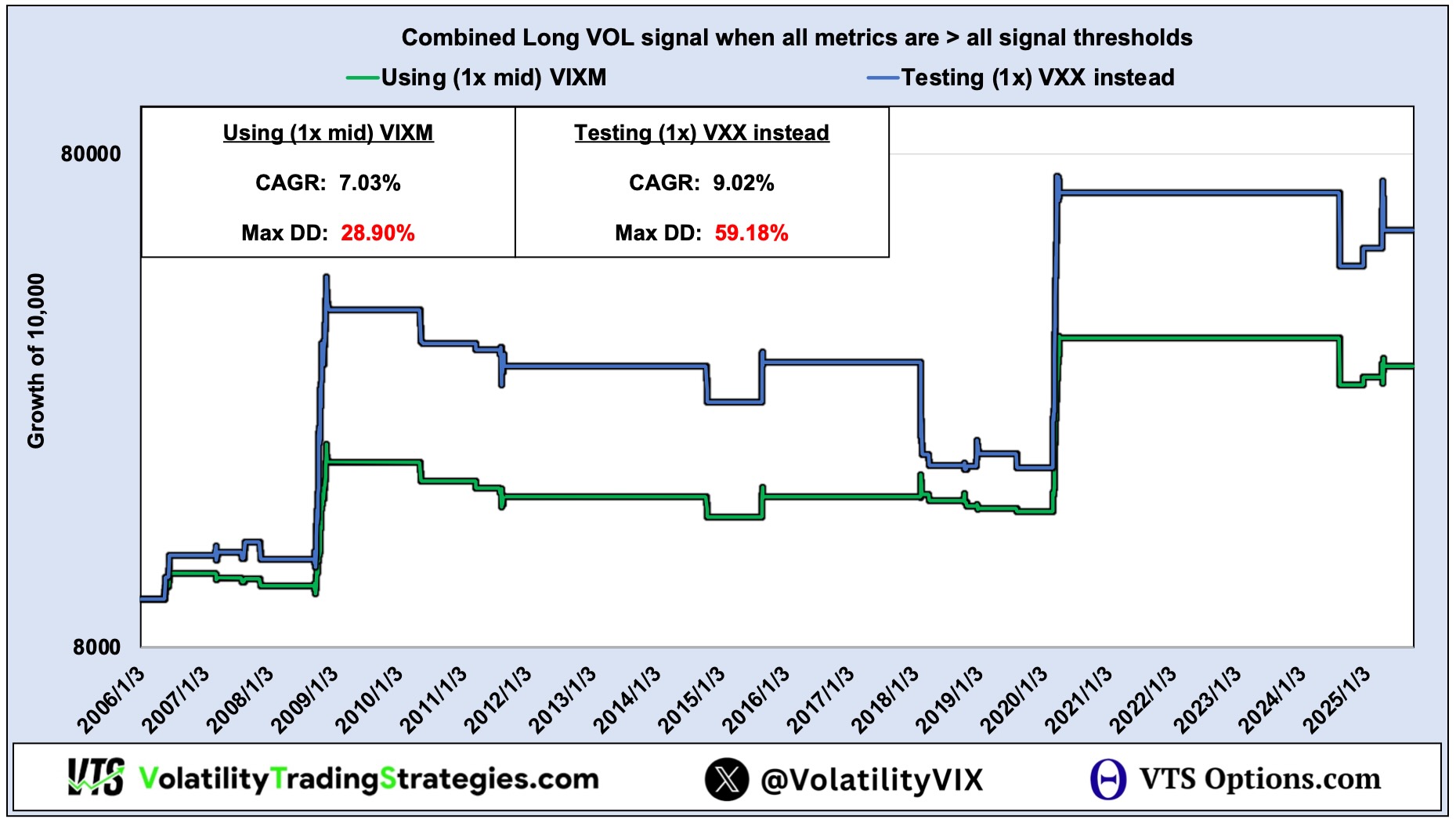

First we'll get an idea for the baseline performance of Long Volatility positions within the Tactical Volatility Strategy using VXZ / VIXM

Those positions only trigger on roughly 2.7% of trading days so it isn't very often. Essentially it's just to capitalize on any major market crash that may happen once every 5-10 years.

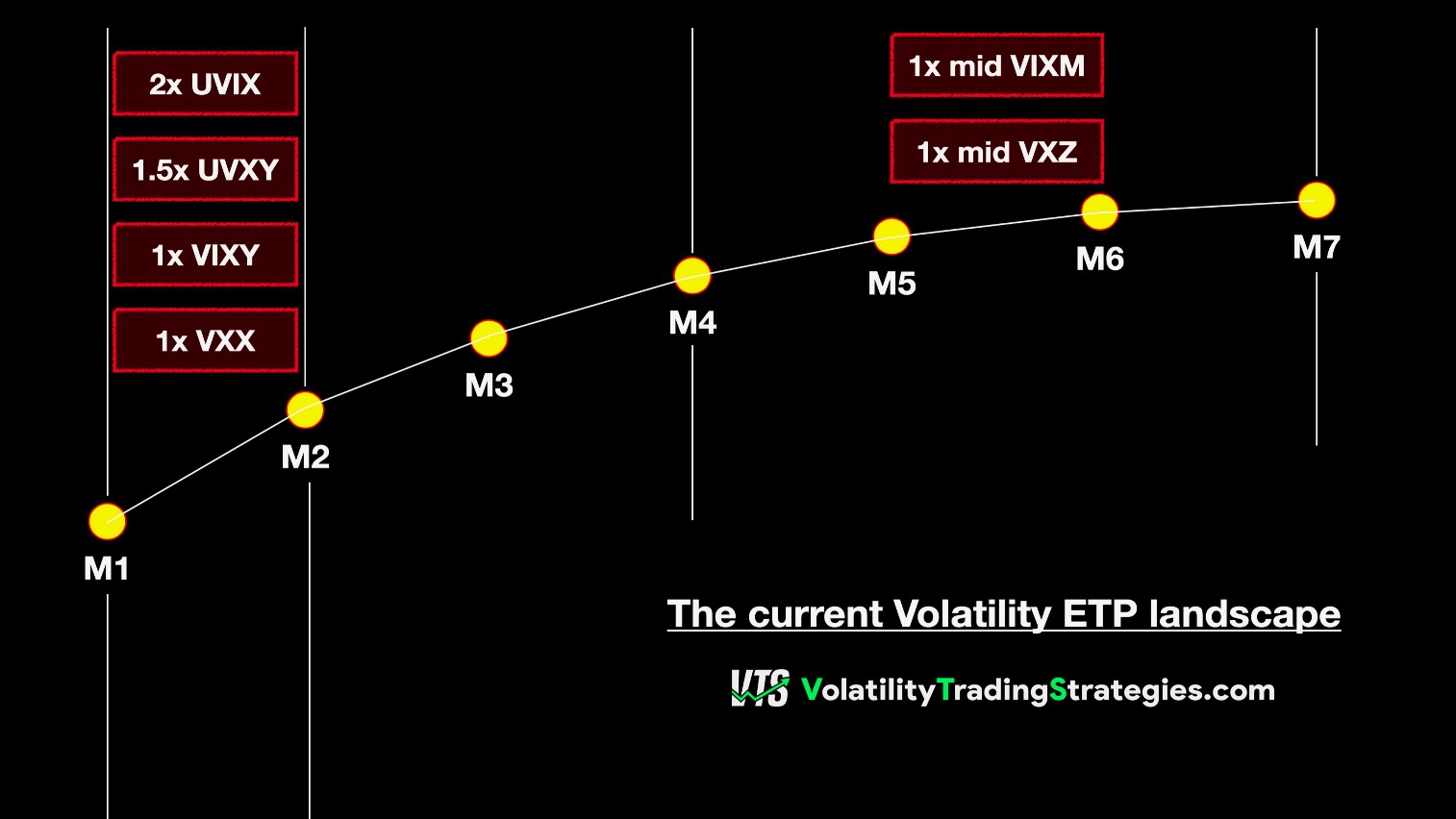

The reason I prefer to use the VXZ / VIXM is because they trade the MidTerm VIX futures from the 4th to 7th month on the Term Structure.

VIX futures that far out tend to be flatter and more stable, they move slower, and they are less susceptible to short term fluctuations in the market.

However, there are several front month M1 M2 VIX futures products that we could use instead. They are also much more liquid than the VXZ / VIXM. If we're talking about the VXX, VIXY, UVXY, and UVIX, they are all more liquid and combined together have over a billion in AUM.

You all know that I place risk management above everything else, so there's no chance I'm going to use leveraged products like UVXY or UVIX. But there's nothing wrong with comparing to VXX right?

This is what VXX performance would look like if we just did a straight substitution instead of VXZ / VIXM

As I mentioned above, VXX does move much faster than VXZ / VIXM so of course we are expecting the potential return to be much higher. The problem though, and is obvious from the chart, that additional performance comes at the extreme cost of large drawdowns.

When navigating through a crisis in the stock market:

1) First, we need to avoid drawdowns

2) After that, we can focus on making money

Clearly using VXX with a maximum drawdown of 59% is a non-starter. It's just too risky and there's too much "give back" when the market flashes warnings but it doesn't actually materialize in a full out crash. That bleed of capital is just unacceptable.

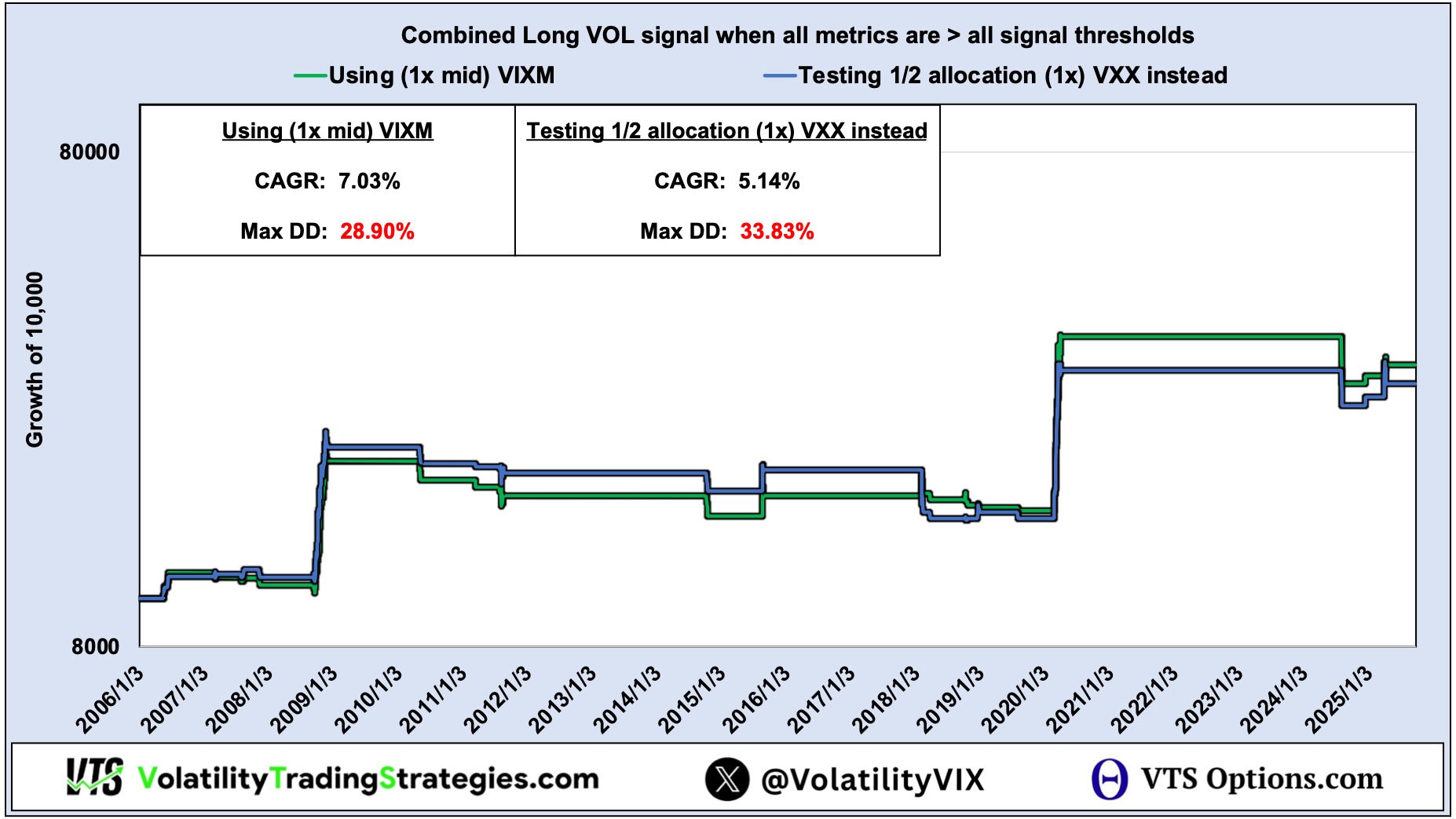

But all is not lost. What if we just used a 1/2 allocation size of VXX?

Although it's still not quite as good as VXZ / VIXM, it is at the very least much closer to something that is manageable in a crisis.

It checks both boxes of reducing drawdowns to an acceptable level, while also making a killer return if the market happens to have a full on recession that lasts a while.

So whether using VXZ / VIXM or the 1/2 VXX, we can be sure that we'll be there to capitalize if history repeats itself. I'm certainly not hoping that happens. Recessions hurt millions of people. As investors though we just have to put those emotions aside and make sure we have a portfolio that is nimble enough to move into Long Volatility when we need it.

We will all feel very bad when the market crashes, but I also want to make money from it when it does

* Feel free to use 1/2 VXX in place of VXZ / VIXM if you prefer.

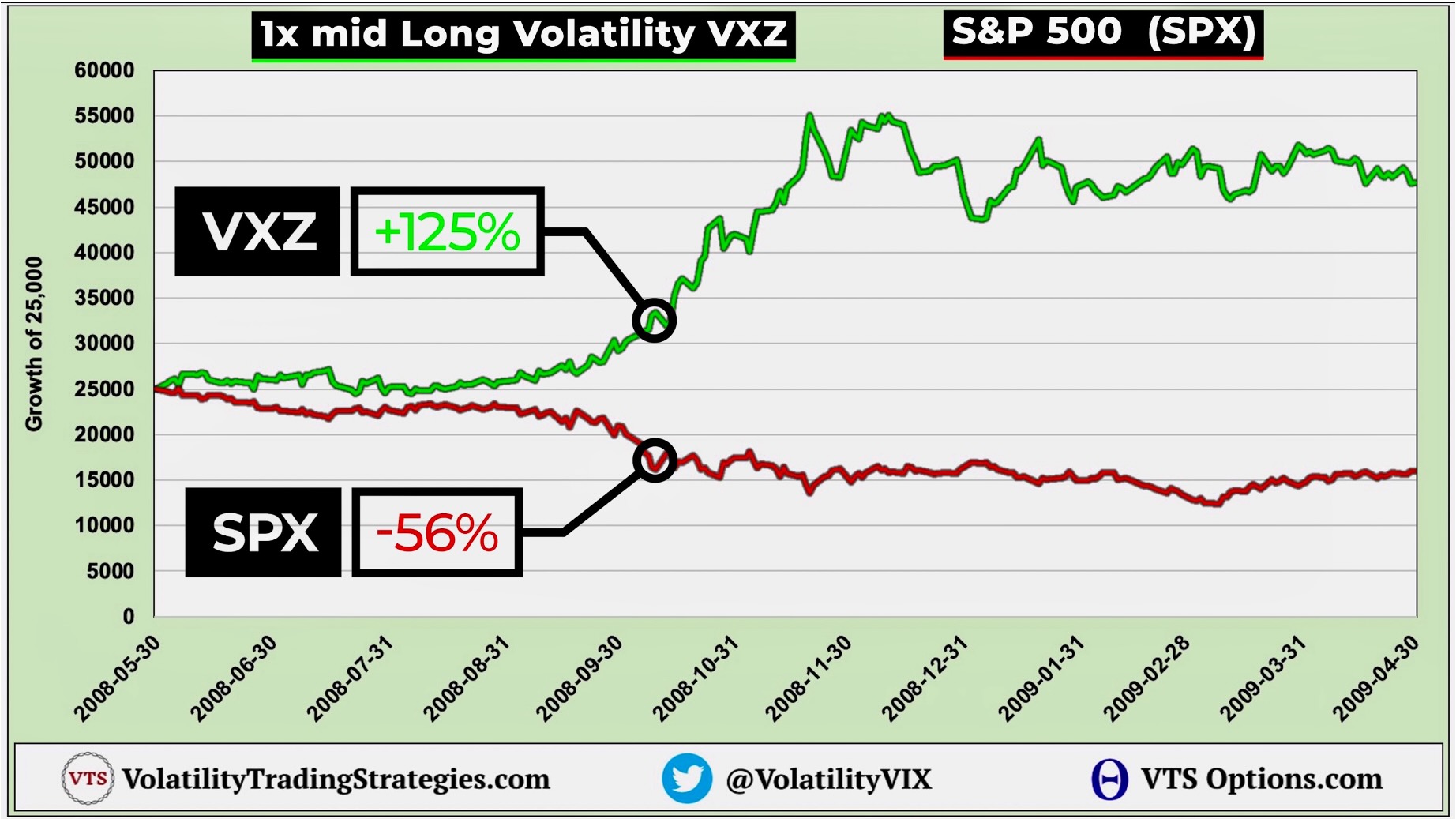

Reminder what happened in the 2008 Financial Crisis:

Take Control of your Financial Future!

Profitable strategies, professional risk management, and a fantastic community atmosphere of traders from around the world.